Global Higher-Education Outlook 2026–27, with U.S. Focus

writing sample, unpublished.

The global higher-education sector enters 2026 in a period of structural demand growth but financial tightening. Worldwide enrollment continues to rise: UNESCO reports a record 264 million students enrolled in higher education in 2024–25, reflecting steadily increasing demand for advanced skills and credentials in every major region (UNESCO, 2025). Even with this strong demand, macroeconomic conditions, geopolitical shifts, and public-finance constraints are set to define the operating environment for institutions in 2026–27.

Global Macroeconomic Conditions

According to the International Monetary Fund (IMF), the global economy is projected to grow by 3.0% in 2025 and 3.1% in 2026, signaling moderate but not exuberant expansion (IMF, 2025a). That means many governments will face tight or flat budgets for higher education, with limited room for meaningful increases in public funding. Emerging economies may continue to drive enrollment, but they too will contend with capital constraints, currency volatility, and inflationary pressures, which could undercut both government support and household capacity to pay (IMF, 2025b).

International student mobility, a key cross-border revenue source for universities, is now more uncertain than at any time since the pandemic. Major destination markets report steep declines in new international enrollments, even when overall international student numbers remain stable. These trends are driven largely by visa policy changes and geopolitical tensions, which put pressure on institutions in countries that depend on international tuition surpluses (Higher Ed Dive, 2025). At the same time, cost pressures are mounting globally: staffing, benefits, ongoing technology modernization, and deferred maintenance are all outpacing institutional revenue growth. As more colleges adopt hybrid and online models, the technology investments required, especially around cybersecurity and AI-platforms,generate recurring costs that make long-term budgeting more difficult.

U.S. Higher-Education Outlook 2026–27

In the United States, these global trends meet additional domestic headwinds: rising operating costs, uneven enrollment recovery, volatile state funding, and uncertain endowment returns.

Revenue, Expenses, and Margin Compression

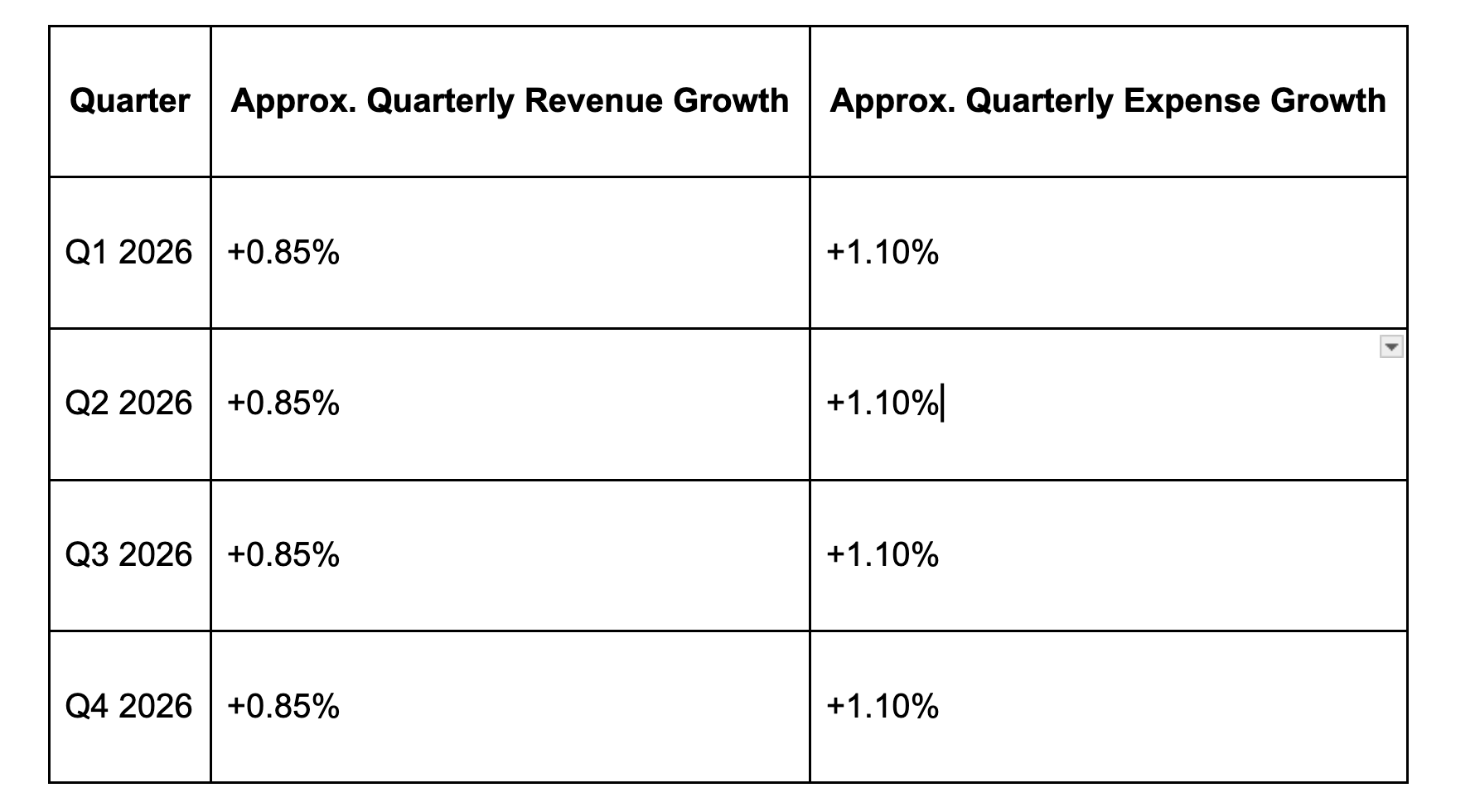

Moody’s projects U.S. higher-education revenue growth of approximately 3.5% in 2026, while expenses are expected to grow by about 4.4%, creating a sustained squeeze on operating margins (Higher Ed Dive, 2025). This financial gap is expected to continue through 2027. For many institutions,especially small private colleges and public regional universities,that means higher tuition, hiring freezes, and potential program consolidations.

A simple quarterly breakdown of Moody’s forecast illustrates the pressure:

Make it stand out

Whatever it is, the way you tell your story online can make all the difference.

Baker, C. (2025, November 18). Moody’s keeps negative outlook for higher education. Bond Buyer.

This pattern, where expenses consistently outpace revenue, erodes institutional flexibility in hiring, capital projects, and student support.

Enrollment and Student Demand

Domestic enrollment in the U.S. has stabilized after recent declines, but the recovery is patchy. The National Student Clearinghouse reports mixed trends: community colleges are showing relative strength, while four-year institutions lag behind. Demographically, a looming “enrollment cliff” driven by lower birth rates since 2008 is projected to become increasingly visible in 2026–27, reducing the pool of traditional-age students.

There is growth potential, though: graduate programs, workforce-aligned credentials, and online learning offerings may provide a structural buffer, but these markets are competitive and require sustained institutional investment.

International Students and Policy Volatility

International students are a key revenue source for many U.S. universities, especially those in STEM and business. However, new international-student enrollment reportedly dropped in several states and campuses during 2025–26, driven by visa policy shifts, geopolitical uncertainty, and growing competition from Europe and Asia (Higher Ed Dive, 2025). For institutions heavily dependent on these students, persistent declines could create budget deficits. Addressing this risk will require diversified recruitment strategies targeting emerging sending markets (e.g., Nigeria, Vietnam, Türkiye, and Latin America) and deeper investment in pathway and institutional partnership programs.

Endowment Volatility and Investment Income

Although endowment performance rebounded in 2024, earlier market losses,especially in 2022,still haunt many institutions. According to NACUBO/Commonfund data, many colleges entered 2026 with caution, opting for conservative endowment draw rates to preserve liquidity (NACUBO, 2025). That caution could limit funding for financial aid, faculty hiring, and capital projects, making it harder to sustain competitiveness in tuition pricing and programming.

Public Funding Outlook

State budgets across many U.S. regions remain constrained as higher education competes for dollars with K–12 education, infrastructure, and healthcare. Many states are projecting flat or even declining real appropriations for their public colleges and universities. Without significant policy shifts, public institutions may have to rely more heavily on tuition increases or cost-cutting measures to stay afloat (Higher Ed Dive, 2025).

Strategic Implications for U.S. Institutions

To navigate the financial and operational challenges of 2026–27, U.S. colleges and universities should proactively:

Diversify Revenue: Expand non-degree credentials, build industry partnerships, grow continuing education, and scale global online programs to offset demographic and funding pressures.

Control Cost Growth: Use shared services, automate administrative systems, and align academic portfolios strategically to reduce overhead.

Rebuild International Pipelines: Invest in recruitment in emerging markets, reinforce visa-support systems, and deepen global institutional partnerships to stabilize cross-border enrollment.

Preserve Liquidity: Adopt conservative endowment spending, actively manage debt, and build reserves to absorb future shocks.

Summary

Global demand for higher education remains robust, but the macroeconomic outlook for 2026–27 is marked by tighter budgets, shifting student flows, rising costs, and volatile investment returns. In the U.S., these global trends intersect with demographic headwinds and declining public support, creating one of the most challenging financial environments in years. Institutions that proactively diversify revenue, modernize operations, and safeguard liquidity will be better positioned not only to survive but to thrive and gain competitive advantage as the sector restructures worldwide.

References

Higher Ed Dive. (2025, November 21). Higher education outlook remains negative for 2026, Moody’s says. https://www.highereddive.com/news/moodys-negative-outlook-higher-ed-2026/806097/

IMF. (2025a). World Economic Outlook Update, July 2025: Global Economy: Tenuous Resilience amid Persistent Uncertainty. International Monetary Fund. https://www.imf.org/-/media/Files/Publications/WEO/2025/update/july/english/text.ashx

IMF. (2025b). World Economic Outlook, April 2025: Growth Forecast for Emerging Market and Developing Economies. International Monetary Fund. https://www.imf.org/-/media/Files/Publications/WEO/2025/April/English/text.ashx

NACUBO. (2025). U.S. Higher Education Endowments Report 6.8% 10-Year Average Annual Return, Increase Spending to a Collective $30 Billion. https://www.nacubo.org/Press-Releases/2025/US-Higher-Education-Endowments-Report-10-Year-Average-Annual-Return

UNESCO. (2025, June 23). Record number of higher education students highlights global need for recognition of qualifications. https://www.unesco.org/en/articles/record-number-higher-education-students-highlights-global-need-recognition-qualifications